Tumult

Futures markets are still the best platform to crowd-source an accurate price for commodities. It rarely makes sense to “argue” with the ongoing, posted prices of copper or oil because commodities are a kind of global collection point for information on their own varying rates of extraction, transmission, and demand. For short periods however, bad information, supply-chain anomalies, or financial speculation can bend and warp commodity prices. These periods can temporarily take price far outside the trading range supported by reality. In the early winter of 2004-2005 for example, a backed-up oversupply of heating oil in the New York-Philadelphia market temporarily took down the global price of oil for about ten days until throughput in that one micro-region could be cleared. More broadly, we know from data that a tremendous volume of financial speculation most surely amplified oil prices during the 2005-2008 period. And it doesn’t help that humans probably expect commodity pricing to be smooth and liquid, when by their very nature commodities are chunky, anchored to earthly constraints.

What are we to conclude therefore as we observe the most recent decline in oil? Well, it helps to understand the context: 2021 demand will still not reach, on an annual basis, the demand levels of 2019. Furthermore, OPEC is still sitting on enormous spare capacity, and global mobility data continues to show that commuting (workplace patronage) is still sitting, generally, 10% below 2019 levels. In other words, unlike previous bull markets in oil, supply is quite artificially tight at the same time financial markets are using the oil market as a way to hedge (play) inflation. The risk in these conditions was rather obvious: should a sudden piece of news arrive that countered either inflation or tight market narratives, structural weakness in the price of oil—should it exist—would be revealed. And that appears to have happened over the past several weeks. Bull markets on strong foundations shake off counter-trend news rather quickly, and keep going. Indeed, during 2002-2008, OPEC announcements that added supply were quickly and serially ignored. But oil has declined for over four weeks now, after setting a high of $85 in late October. The market was easily pushed around by the threat of oil inventory releases—which, it must be said, are rather minor and toothless. A big bad bull market would not have been so cowed.

{kind=link}

Friday’s oil price crash however cannot be utilized just yet, in either bullish or bearish arguments. A classic One Day Wonder, the singular $10 decline offers little useful information. But what is notable is that oil crashed after falling for a month. Now sitting below $70, the case for a strong and enduring bull market would be strengthened best by a quick recovery that now shakes off both the inventory releases, and the Covid variant threat. The Gregor Letter takes the view such a recovery is unlikely to happen. Not because of renewed Covid fears, but because the market had gotten way ahead of itself.

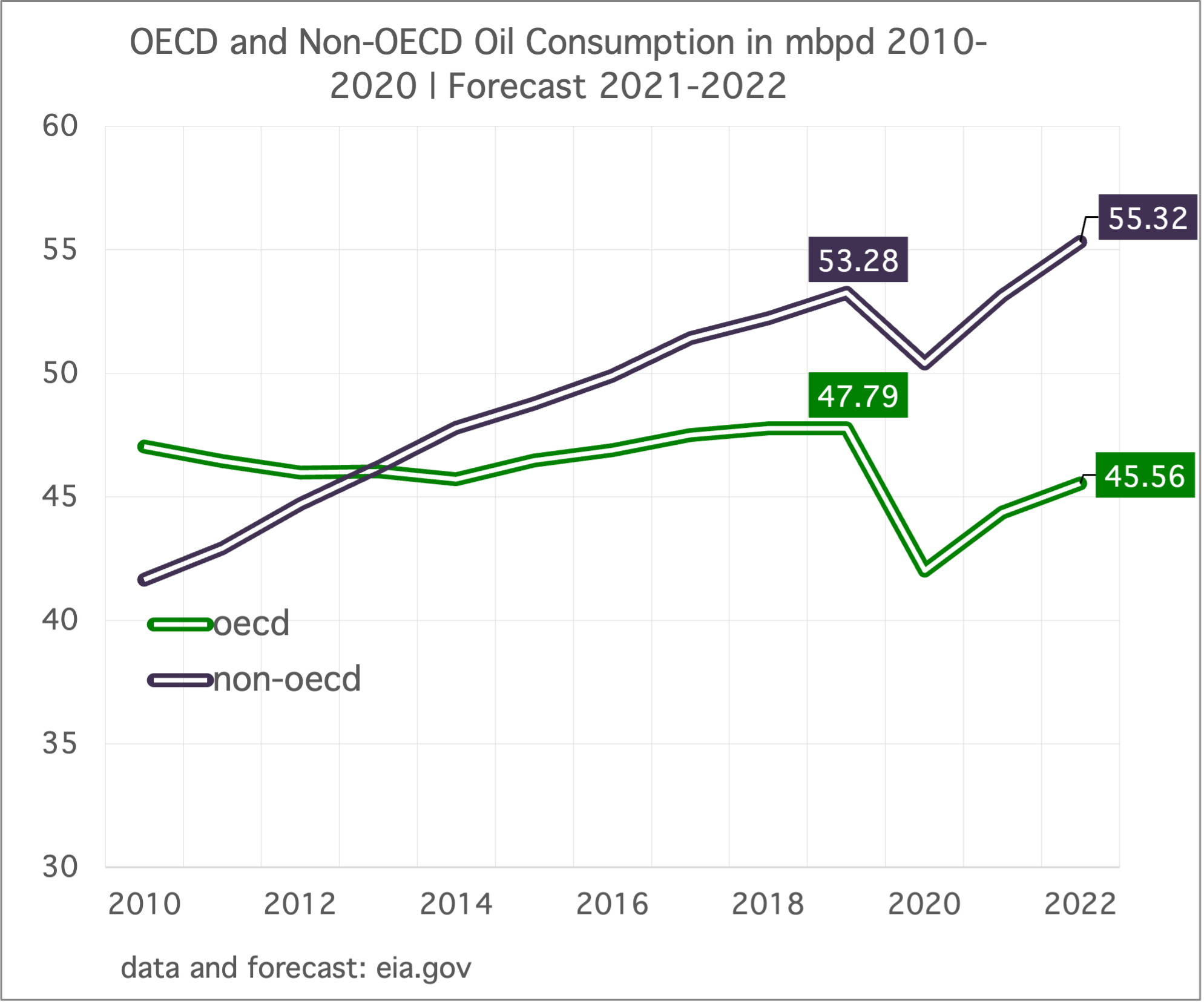

Let’s consider another context: the trajectory for oil demand in a post-pandemic world. In the chart below, notice how OECD demand never makes it back to the 2019 high, and is now acting as a drag on global demand growth even as Non-OECD demand goes forward. As previous letters have pointed out, OECD demand supported global demand for many years not by rising, but simply by refusing to decline. That phase is now very much over. For global oil demand to rise, Non-OECD consumption growth will have to outrun OECD declines. An easy prediction: OPEC spare capacity will hold firm, if not increase in the years ahead. That’s the most obvious outcome to a no-growth market, that will also eventually enter sustained decline.

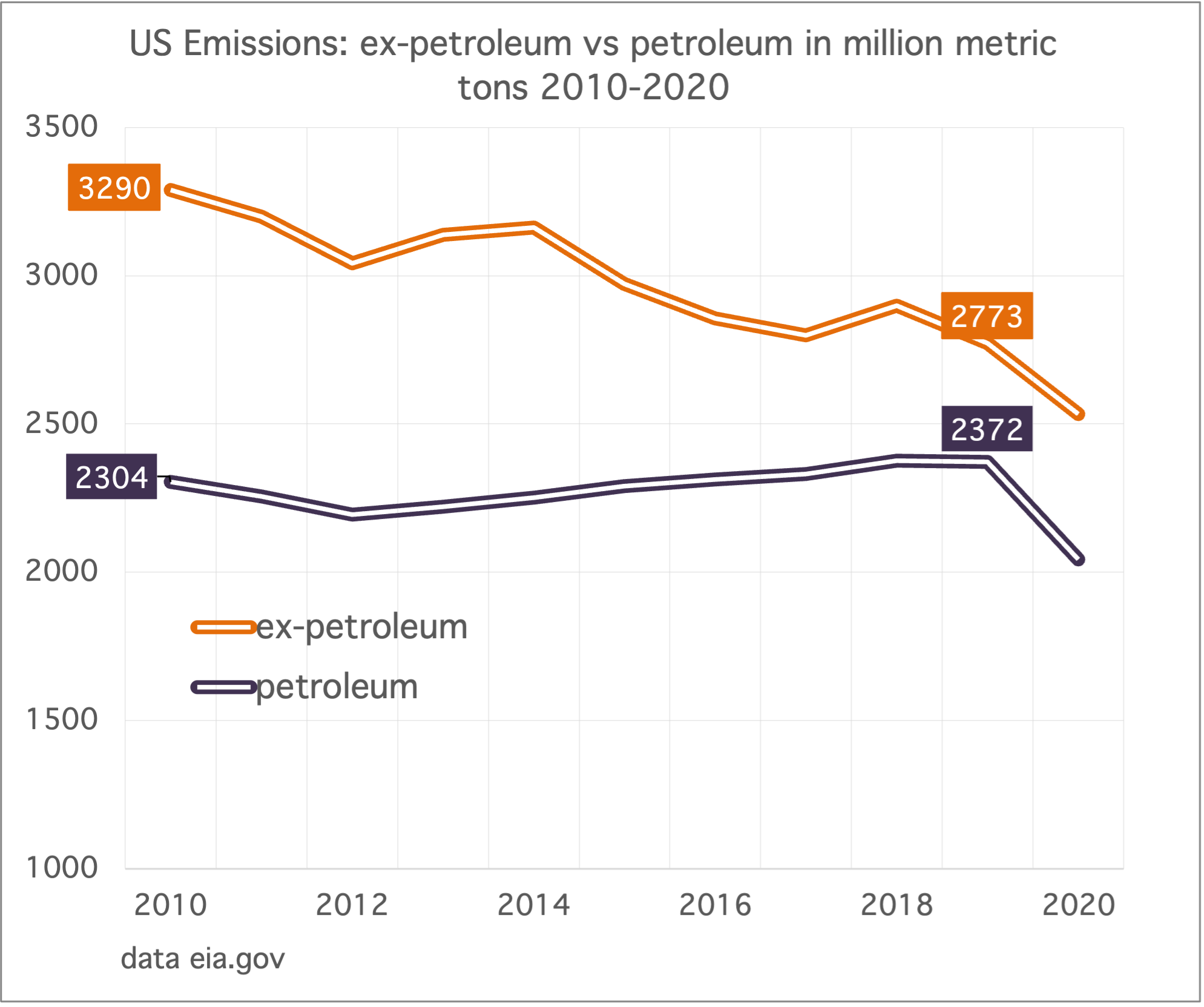

US emissions ex-petroleum are in a well established, decade-long downtrend. The genesis of the downtrend is also well understood. How it played out over the past ten years is quite visible. And, the prospect for its continuation—even absent a new policy push—is excellent. Let’s briefly describe these in order. The first term Obama administration asked itself productive questions, wondering how to set such a trend in motion that could gather its own momentum and endure in the years once that team was out of office. And so began a major policy push to kick-off solar deployment. This triggered the learning curve (declining costs) at a most fortuitous juncture, when the post-war coal fleet neared retirement. Ground-up efforts from the Sierra Club, and top down policies from the EPA, then concurrently got to work on coal—just as coal was at its most vulnerable. Finally, all the hoped for cost-crossovers occurred in wind and solar, and now costs are declining also for storage. Hybrid systems, in which new generation from wind or solar (or both) are paired with storage are becoming the norm in the US.

The chart depicting the divergence between petroleum and ex-petroleum emissions is going to become more pronounced in the next few years, and the two series are likely to crossover. The momentum in ex-petroleum is not shared however in petroleum emissions. Ignoring the 2020 data point, you can see that petroleum emissions were actually a touch higher in 2019 compared to 2010. Why? Because the US had no credible plan to reduce these emissions, and still doesn’t.

The Transport and Climate Initiative, which would have functionally raised a carbon tax on petrol, has now fallen apart after Connecticut and Massachusetts withdrew their support. Rhode Island quickly followed. What’s useful here, educationally, is that the 13 state coalition which formulated this plan is politically blue, if not deep blue. Thus, we have another example of revealed preference when it comes to climate change, and people’s cars. States veered away from the plan when petrol prices rose substantially, placing political pressure on incumbents. And that placed pressure on state lawmakers, who gave feedback to their governors that such plans could not make it through state legislatures. As The Gregor Letter has tirelessly pointed out, the barrier to undertaking action on existing cars, their emissions, and petrol consumptions in blue states does not come from Republicans, but rather, from Democratic voters who agree with macro, top-down themes around climate change up to the point of any proposal to tax their driving. This is why Democrats both at the state and federal level are sticking with the general plan to decarbonize transport through EV adoption, rather than any disincentives on existing road fuel emissions.

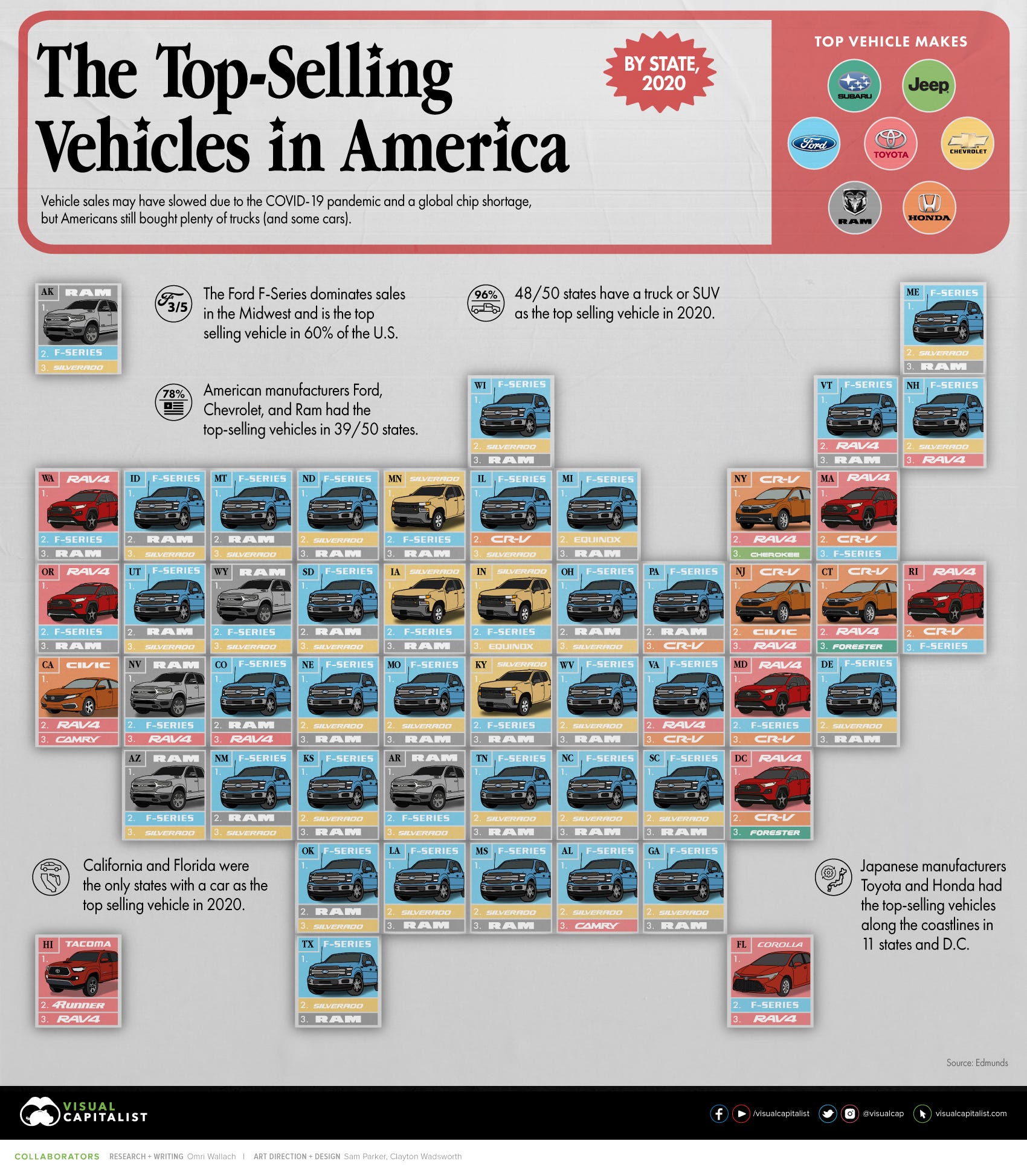

It’s increasingly uncertain whether Tesla has the right model line-up for what comes next in the US EV market. Starting about one year from now, Ford will release the E-150, and Rivian will also be slowly ramping up to broader production of its wildly anticipated pick-up truck, the R1T. Both companies appear to have absorbed a deep truth about the US car market: Americans hate sedans, which have been in a steep downtrend for over a decade. Ford in fact started phasing out sedans altogether in 2018. What do Americans love? Trucks, yes. But even moreso, mini SUVs—which readers outside the US can best understand as a vehicle with the wheelbase of a sedan, but with a more elevated carriage and a crucial fifth door, a hatchback. Popular examples are the Honda CRV, the Toyota RAV4, and the Mazda CX5. Accordingly, global automakers are gearing up to flood the US market with electric versions of this vehicle type, also known as the crossover. Kia’s Niro EV, Hyundai’s Kona EV, and the Volkswagen ID 4 have already landed in the American market, with many more to come. To make the point clear about American preferences in car types, here is a chart of the best selling vehicles in each state.

As you examine the above chart, how would you design an EV strategy for your car company? This appears to be a question that Tesla failed to ask itself. What does Tesla have to offer against this truck and crossover drenched market? Many Tesla supporters are certain the Model Y is the best offering in the crossover market. But the Model Y is not a crossover. It is really a bulky sedan, and does not have a vertical style hatchback but a fifth door that really looks much more like a trunk. That door is not in any way “like” the kind of hatchback that enables suburbanites to load a typical variety of furniture, gardening equipment, and other oddly shaped items into the rear. All this said, the Model Y has sold very well so far. So have Tesla sedans. That’s right! Even as sedans died in the US market, Tesla sedans have done extremely well. Why? The explanation is pretty obvious: if you wanted a full 100% battery electric vehicle the past five to six years, Tesla had one to sell you.

Past performance is no guarantee of future results. Tesla’s Model Y was just brutalized in a recent performance review, and the writers focused on an ongoing area of concern: problematic safety issues, and the failure of the company to deliver on repeated promises of self-driving capability. Let’s pause here and observe that other global automakers are far less ambitious. Tesla prefers the cutting edge, and that too is a viable strategy. But what model is Tesla going to offer in the US market to compete with the flood of EV crossovers?

More foreboding is the very poorly conceived cybertruck, which is really a fantasy vehicle that looks like it would appeal to an oligarch, but not a family in Columbus, Ohio. The cybertruck was announced before Ford’s plans were known for the E-150, or GM’s plans for the EV hummer, or the blockbuster partnership between Rivian and Amazon. One wonders: would Tesla envision the cybertruck today, given these commercial developments among its competitors? It would be impressive, frankly, if Tesla pivoted here, and actually cancelled the cybertruck, which is already delayed until early 2023. As we move into a more competitive EV marketplace, one can discern an understandable blind spot with Tesla’s strategy: having had the EV market all to itself for a number of years, it got used to the market devouring the models it chose to build. That phase is now over, and Tesla needs to digest a change in the landscape.

{kind=link}

Inflation due to supply constraints is at the forefront of markets right now, but best not to forget demographics. India now joins China and the US as it sees fertility rates drop below the replacement rate. Once upon a time the world was concerned, with some justification, that population was exploding past carrying capacity. This conversation dominated economic thinking in the 1970’s. That equation is now entirely turned on its head. The reason: upgraded living conditions mean parents can invest in a fewer number of children, once they are assured that child mortality is receding as a threat. This has been the story of the past two decades, and that’s why previously sky high fertility rates in countries like India are not merely falling, but crashing.

SP500 earnings estimates continue to guide higher for next year, but at a slower pace. Analyst consensus earnings, which grew at a powerful 47% this year (coming off a low base) will settle down next year, growing at just 7.7%. The data is tracked by Yardeni Research and can be found here (opens to PDF). While the recovery expands, however, and stock prices continue to advance, an old and familiar dynamic is coming into play: as asset prices rise, their sensitivity to counter-narrative news is heightened. That dynamic is probably going to reveal itself more frequently now, and especially next year, as the tumultuous nature of energy transition and industrial expansion introduce further volatility into markets. Readers are encouraged to review previous letters, warning that commodity and material shortages could themselves be disruptive in 2022. Indeed, this will probably form a large component of the outlook, when published next month.

—Gregor Macdonald

The Gregor Letter is a companion to TerraJoule Publishing, whose current release is Oil Fall. If you've not had a chance to read the Oil Fall series, just hit the picture below.