The China Bid

Weakening industrial activity and rising food price inflation are currently plaguing China, and that’s extremely concerning for the global economy. China is a country that has grown far above trend for several decades and typically this pressages a secular slowdown to a more normal rate of growth. Worryingly, however, this inevitable maturation appears to be unfolding into the face of a cyclical slowdown too—as flagged by the deep slump in China’s auto market starting last year—and to make matters worse, a third layer of deceleration: the trade war. The time has come therefore to talk about China, and the impact its slowdown could have on energy markets, deflation, and the US economy.

For twenty years now China has provided the bid in global resource markets, and every corn farmer, oil producer, copper miner, and coal extractor has feasted on China’s demand strength as the rest of the world, the OECD mostly, has gone quiet. But it’s not just cement making, steelmaking, and winemaking businesses that have been able to survive, if not thrive, as China’s industrial revolution pressed onward. Much of the European high-end industrial sector too has managed through a terrible decade of domestic growth by supplying all the sophisticated engineering and power equipment China required to complete its development of cities, tunnels, airports, and rail networks.

Apparently, however, the world simply forgot how necessary The China Bid had become. Massive, widespread, and globally dominating it was perhaps easy to take for granted but even the investment and money management business came to rely on China’s long expansion. Indeed, it was well accepted—especially after the great recession—that aging populations in the West would, through their investment choices, have to borrow growth from China and the rest of the Non-OECD to earn a rate of return.

What appears to be happening now is that the China bid is being withdrawn. Here, I use the word withdrawn not to mean an evaporation but rather a steady weakening. There is still a bid, but it’s a bid for less volume. And, in the nature of market bidding this withdrawal has not a small but rather profound effect on price. Which brings us to energy, and the US economy.

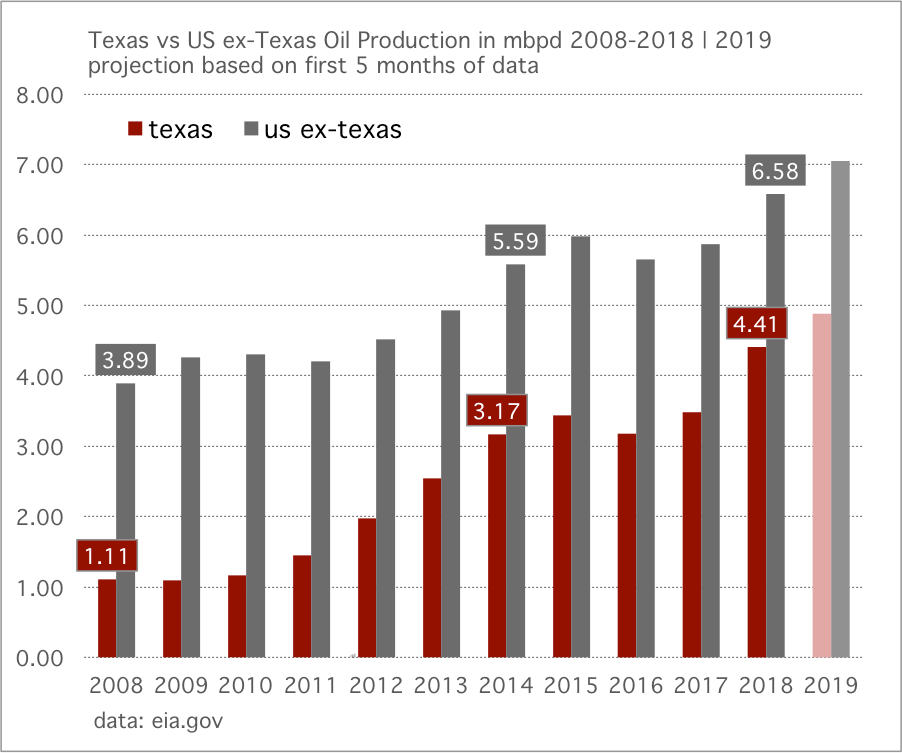

As you’ve likely observed, the US oil and gas industry has worked itself up to ramming speed. Over the past decade, oil production alone has soared from a low of 5 million barrels a day (mbpd) to over 12 mbpd. The EIA expects oil production to move above 13 mbpd next year. In addition, the US has expanded its industrial base around this growth—not merely in service of the extraction of raw oil and gas—but also through a newly beefed up LNG and petrochemical export complex. To put it plainly, the US oil and gas industry has got itself into perfect position to exploit an extended phase of higher global growth, all funded by new units of fossil fuel. You can see the problem that would develop, however, if that phase were not to materialize.

This Spring, global interest rate markets sent the first warning that global growth was about to slow. As usual, the rate decline was initially doubted and denied. Presently, as rates have moved even lower—with many domains now seeing negative interest rates—the move has been reacted to with anger and bargaining. You have already guessed what comes next: depression, and acceptance. But we are not there yet.

Recessions and stock market crashes are often preceded by investment bubbles. The behavioral reaction to the bursting of those bubbles, typically, becomes the cause of the recession. The China situation strikes me as something different altogether. For, it may be less the case the global economy has been marching along through a bubble (contra the view of those who see bubbles everywhere), and more the case that China, whose industrial revolution came very late in the 20th century, was a singular, one-time growth event that’s now ebbing, and won’t be repeated. And here, ebbing may not be strong enough a word. If so, then a large deflationary wave has started to wash over the global economy, and it will not be countered effectively by interest rate cuts from Western central banks. Indeed, given the very low rate of growth already established in the OECD, there is no domain anywhere on the planet that can counter China’s transition to a late phase, mature level of growth.

Let’s consider some recent developments:

The oil and gas services index, the OSX, never recovered after the 2014 oil price crash and recently has fallen to lifetime lows, as expressed by OIH the Van Eck Oil Services ETF.

In addition, the ETF which best tracks the Standard and Poor’s US oil and gas exploration and production sector, XOP, has also fallen to lifetime lows. This seems important, and here’s why: both OIH and XOP have significantly undercut even their lows seen in 2009, during the great recession.

Globally, Germany and the United Kingdom, and Europe more generally, appear to be entering recession. Germany’s ten year government bond trades at a negative rate of interest. And, the European auto sector has been hit hard by the China slowdown. Meanwhile, the entire European banking sector is groaning, or rather, shrinking under the pressure of negative interest rates and withering economic strength.

As so often is the case, disturbances in the rest of the world take time to arrive in the US. This routinely gives the false impression to US based investors that the US economy is impervious to such shocks. But, we are only six months out from the first concerning appearance of the global deflationary wave, and already the US Federal Reserve has pivoted entirely from previously expected rate hikes to a series of expected rate cuts. It would appear the transmission mechanism from China to Europe and now the US is not so slow after all.

I spent some time this weekend reading a 2015 report from the Dallas Federal Reserve covering the effects of the 2014 oil price crash on the Texas economy. Brief takeaways: Texas today is a far more diversified economy, obviously, compared to its former self in the 1980’s when a devastating oil bust took down the housing market and a bunch of banks. The alternate view, however, is that oil production has grown quickly and to a very high level in Texas, even in the wake of the 2014 price crash. Indeed, after pulling the most recent data you can see that Texas, unsurprisingly, remains the key driver of the nation’s oil production growth. (See chart below). When you add the petrochemical industry, and also exports of LNG, the fossil-fuel energy industry of Texas is quite substantial. (Wind power is also a newly substantial industry in Texas, and that’s important to acknowledge). If a useful signal is being sent by share prices in this sector, OIH and XOP, then a China-driven oil bust will hit the Texas economy with notable force.

So how is China’s economy doing, right now? Early indications show that its auto market slumped for the 13 month in a row, in July. According to CAAM, the China Association of Auto Manufacturers, the total market is now down -11.4% through the first seven months of the year, compared to 2018. The weakness is even taking a small bite out of EV sales which, although strong, may “only” grow by 42% this year. In addition to broadening industrial weakness, food price inflation—which has its genesis in the recent cull of its hog population in the wake of swine fever—has started to appear. This hits Chinese consumers at both ends; and, frankly reminds me of some of the pressures that landed on US consumers in 2005-2007 when energy prices rose as house prices started to fall. To put it mildly, the Chinese consumer is going to be quite constrained for a while, and this will greatly impact the country’s demand for road fuel.

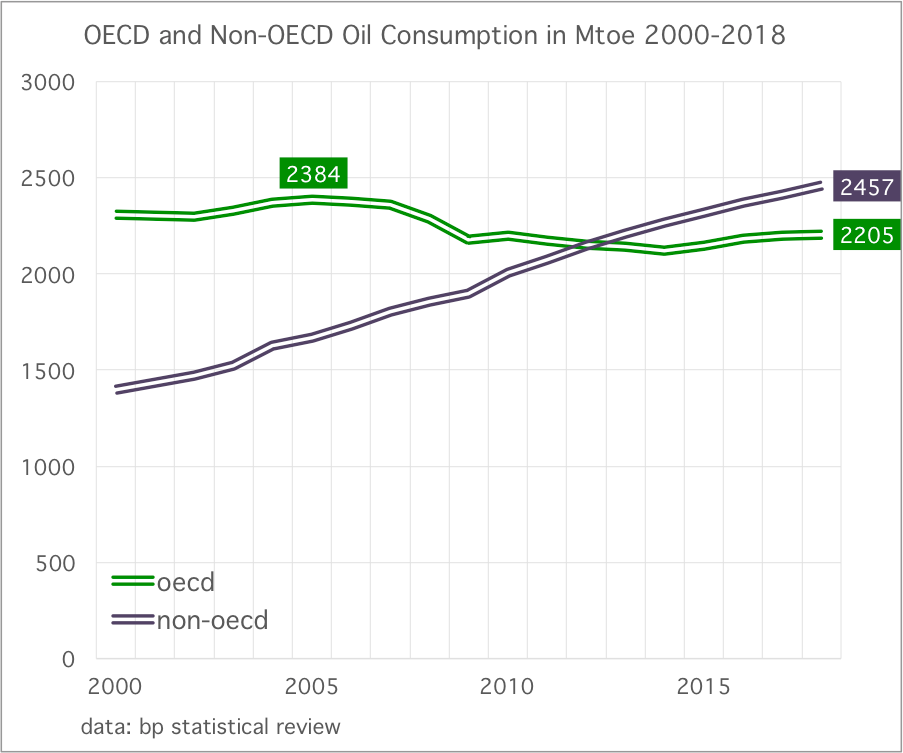

Just to remind: oil consumption peaked nearly 15 years ago in the OECD. And really, since 2010, the Non-OECD as led by China has been in total control of global oil demand. Normalization of China’s economic growth to align with that of all previously maturing countries will eventually be absorbed into the smooth running of the global economy. The problem is that the world came to rely on China’s high and unsustainable rate of growth, and transitioning from one domain to the other, right now, will be painful—and not just for the oil and gas industry.

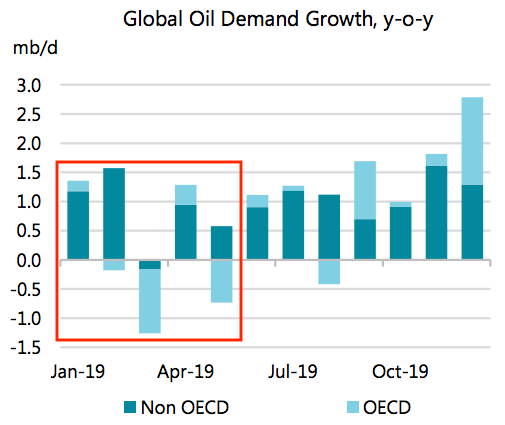

The IEA oil forecast has been on the defensive all year, falling well behind a major deceleration in demand growth. The Gregor Letter forecasted in February that the consensus view of 1.4 mbpd of growth was far too high for 2019, and that risk pointed to growth at half that level, of just 0.7 mbpd. On Friday, IEA lowered its forecast again, to 1.1 mbpd. Again, that’s not enough. The chart below, from Friday’s Oil Market Report, shows how the mistake is repeatedly made, as the agency can't let go of a rebound-thesis for which there is no evidence or probability. Here, I’ve put the first five months in a red box (for which the data is now available), showing the outright declines in the OECD, and the very weak growth in the Non-OECD.

Now: consider the IEA forecast for the final 7 months of the year in light of the darkening outlook for the global economy. Why would you do that? Why wouldn’t you build in the very serious problems in China and Europe into your outlook? I must say, the IEA’s analysis has been absolutely terrible the past two years on every topic from wind and solar growth, and now, oil demand. It’s almost a certainty now that oil demand growth will come in below 1.0 mbpd this year. And price risk remains very much to the downside.

—Gregor Macdonald, editor of The Gregor Letter, and Gregor.us

The Gregor Letter is a companion to TerraJoule Publishing, whose current release is Oil Fall. If you've not had a chance to read the Oil Fall series, the single title just published in December and you are strongly encouraged to read it. Just hit the picture below.