Great Games

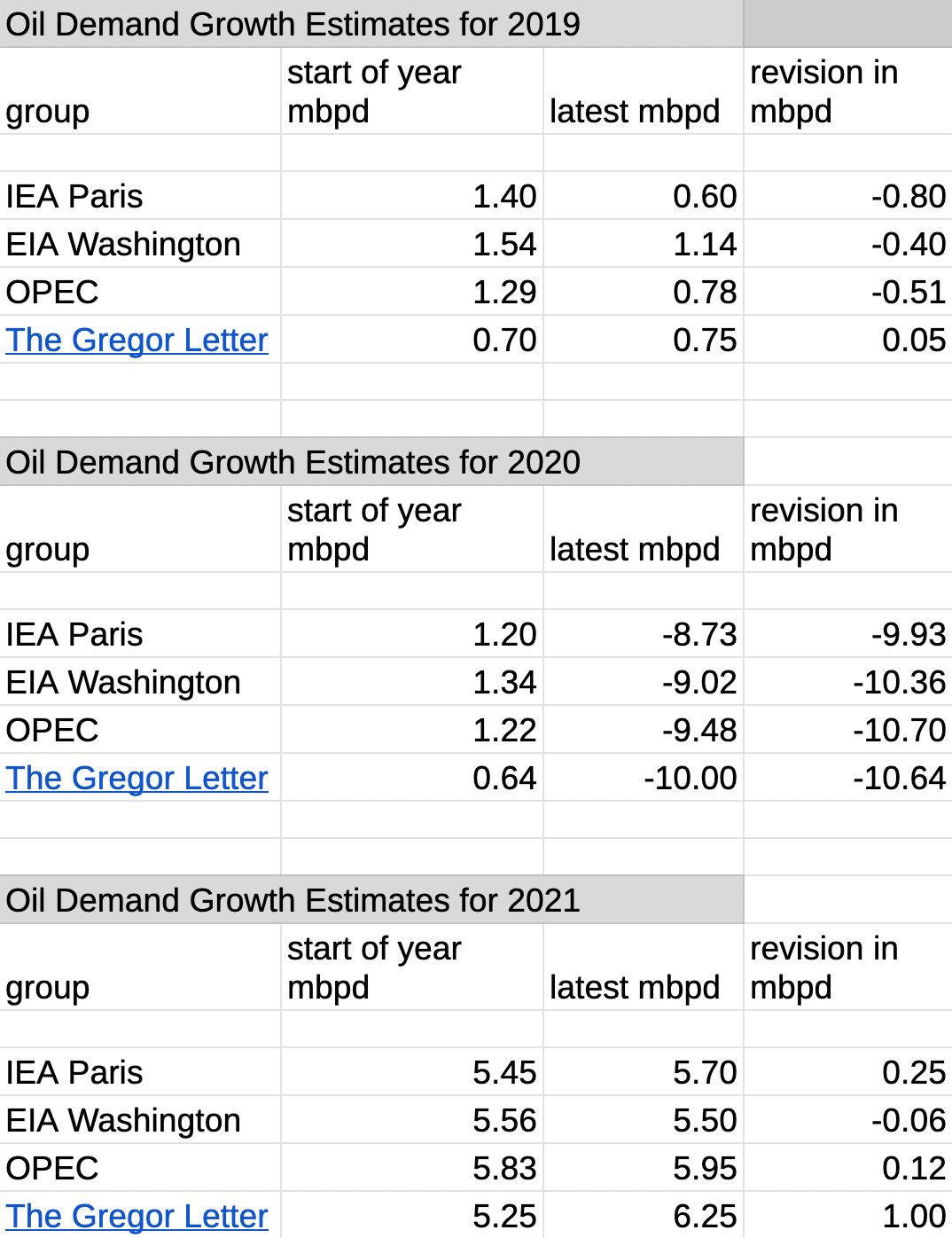

OPEC and IEA have increased their estimate of 2021 oil demand as the macroeconomic picture brightens. Both forecasts move in the direction of The Gregor Letter estimate for this year, with OPEC in particular now at 5.95 million barrels a day of growth. The current Gregor Letter forecast stands at 6.25 mbpd. Amidst a global economic recovery, US demand is now the biggest driver of these increased calls. But there’s equally a slight drag from Europe where the combination of higher than expected EV sales, with a slower pace of economic recovery, is more effectively constraining the liquid fuel rebound. Using IEA as our baseline, at 100 million barrels a day of absolute demand in 2019 (actually, now 99.73 mbpd), global oil demand this year will recover to 96.7 mbpd. That makes the math easy: 2021 demand will reach 96.7% of the 2019 level.

In the table below, which records year-over-year demand changes only, the final estimates for changes 2018 -2019 are listed. In the next update, the 2019 portion will be dropped and the 2022 section added. Just a brief comment, though: now that we are halfway through April, it’s likely the oil market has largely priced in this year’s demand rebound. Importantly, there really is no supply side constraint at all currently in the oil market. OPEC has at least 5.00 if not 6.00 mbpd of spare capacity. And new world oil (the US mainly) remains the beneficiary of a long decade of investment. The only game left in the oil industry is to manage the end of growth.

Oil and gas are no longer the focal point of geopolitical pressure, or competitive action. The new great game centers on specific natural resources, and the productive capacity required, to serve electrification. In the past few months we have witnessed nothing less than a panic by both governments and corporations to more effectively secure lithium supply, battery manufacturing capacity, and semiconductor supply-chains. Let’s list some key examples. Volkswagen panicked, and locked up nearly a decade of battery production capacity with Northvolt. Under threat from US enforcement of a trade secrets dispute, LG Energy Solutions and SK Innovation of South Korea settled their differences, thus smoothing the path to supply batteries to both GM and Ford. Separately, the Bureau of Land Management gave the green light to the Thacker Pass lithium mine project. The open pit project will greatly damage open range land in northern Nevada, and will require sulfur to separate the lithium. It’s hard to imagine such an approval going forward without the extreme urgency surrounding EV adoption. Relatedly, Rio Tinto started its innovative recycling of lithium from existing tail waste in Boron, California. Albemarle, which operates the only lithium mine currently in the US, is embarking on a doubling of production. Finally, there is a rather serious semiconductor problem globally, as there is not enough capacity to meet demand. This means the highly engineered equipment made by companies like Applied Materials, Lam Research, and ASML—which actually produces the chips at contract manufacturers like Taiwan Semiconductor—will itself need to be manufactured, and then installed. There’s a decent chance the global chip shortage will be semi-permanent for years to come.

One is reminded of the Viking period, in which raiding parties set forth ostensibly to plunder gold and silver, but in actuality were in search of arable land. A clashing of vestigial, legacy goals with new needs. What’s really needed is the land; or in our case, batteries and chips. To extend this idea one more step: the search for the vestigial resource, oil, is now over. The future will see oil extraction contract to the lowest cost producers, mostly in the Middle East, as they serve a dwindling customer base. By contrast, the winners of the new great game will be the chip designers, the battery innovators, the grid algorithm composers, and material scientists. Indeed, we are probably on the threshold of a new wave of interest in geology and applicants to mining schools, with a concurrent wave of students pursuing material science. Worth mentioning: when the first theories about a world running on solar were taken seriously 10-20 years ago, scientists at MIT began to examine the potential for material upgrading, should certain critical materials become uneconomic or too scarce to procure. Here is a good review of the critical materials the US government now worries about, as the country faces new technological needs.

One super-theme to track is the coalescence of clean energy both as an input, and an output, in manufacturing. Now that wind and solar are the cheapest energy on the planet, domains that optimize their use as energy inputs to production will ultimately become the favored choice for product designers. Apple, Nvidia, GM, Ford, Tesla, and Panasonic and CATL will all eventually migrate production to clean energy centers. Or, they will establish those centers more fully, where they are currently located. This analysis of the Volkswagen-Northvolt partnership by Colin Mckerracher of BNEF hits on this exact point.

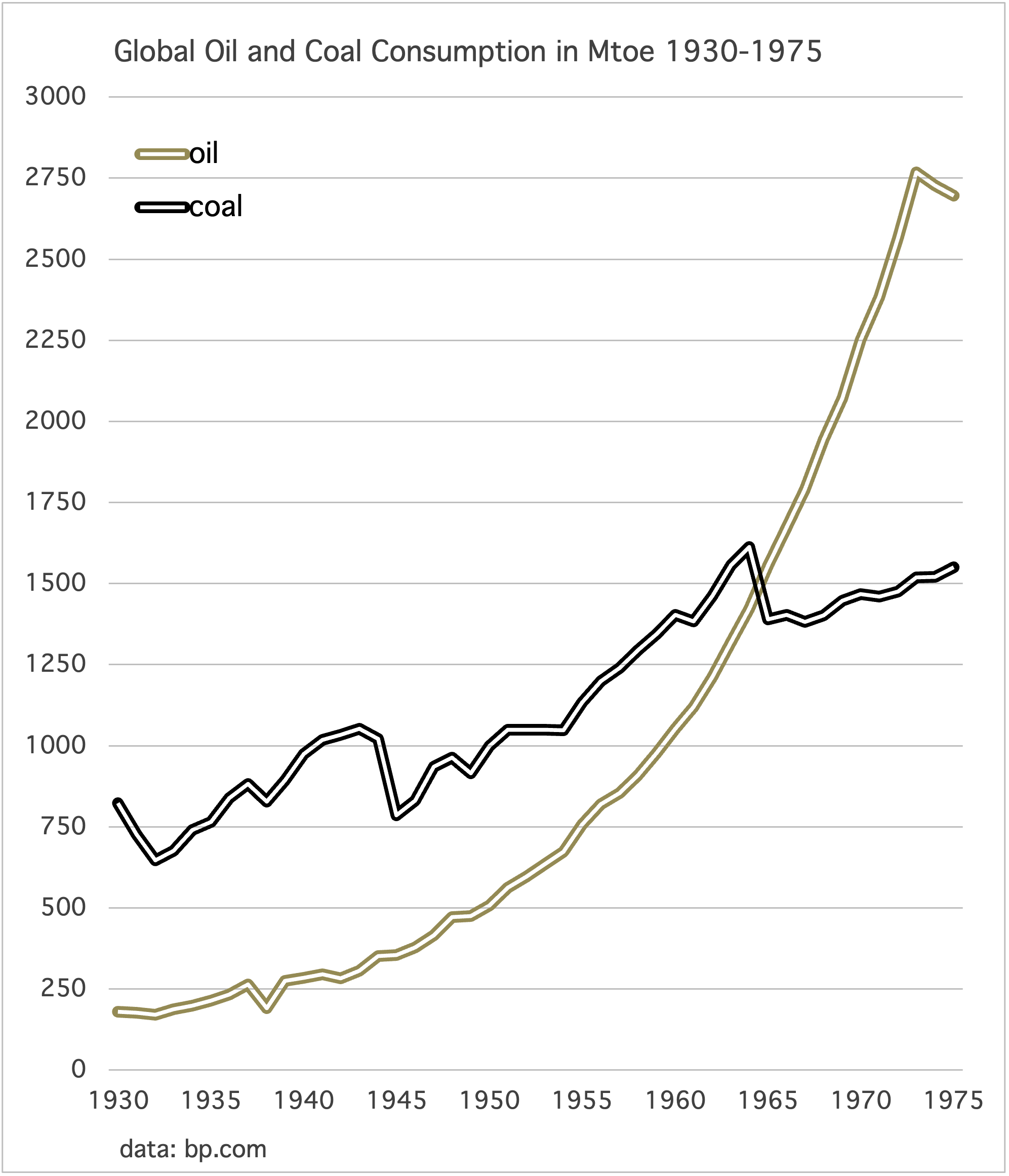

Faultlines and the tectonic plates are therefore on the move. Global production historically has been about access to coal, gas, oil, and low cost labor. China put both of those factors together in spectacular fashion between 1980 and 2010 as it adopted coal and drew in cheap labor from the countryside. While the marshaling of cheap labor globally will continue for a while (see: the Lewis turning point) global electrification is more likely to scoop up populations into a different kind of work. If clean energy is now the most competitive energy source, then it will become so everywhere. Here, we should think about oil’s original adoption curve, when coal was displaced. Because something similar is now in store for clean energy:

As you look at the grand upsweep of oil into the global energy system (doubling, for example, from the start of WW2 to 1950) consider all the exploration, capital expenditures, and organic investment that gathered around oil’s adoption. Those same self-organizing dynamics are now starting to gather around clean energy. According to Benchmark Mineral Intelligence there are now over 200 battery megafactories planned or under construction. They represent a future path dependency for electrified transport. And at this point, frankly, one has to chuckle at the prospect that many remain “doubtful” about the global adoption of EV. The entire auto industry is transforming its capital equipment base! By 2030, any new ICE vehicles produced will mostly be on bespoke terms; the global inventory of charging stations still offering a petrol pump will have greatly dwindled; and every new power plant will be renewable-sourced with a companion battery. There is no longer any mystery or uncertainty about our future direction. The world is moving towards a condition of locally produced energy, that will be manufactured along precise, digital terms. While demand for resource extraction will now migrate to a very different set of materials, our energy transition will absolutely shift pressure towards human resources. Accordingly, the future of the global energy system will look increasingly like the technology sector, where demand for the best minds and innovation will be substantial.

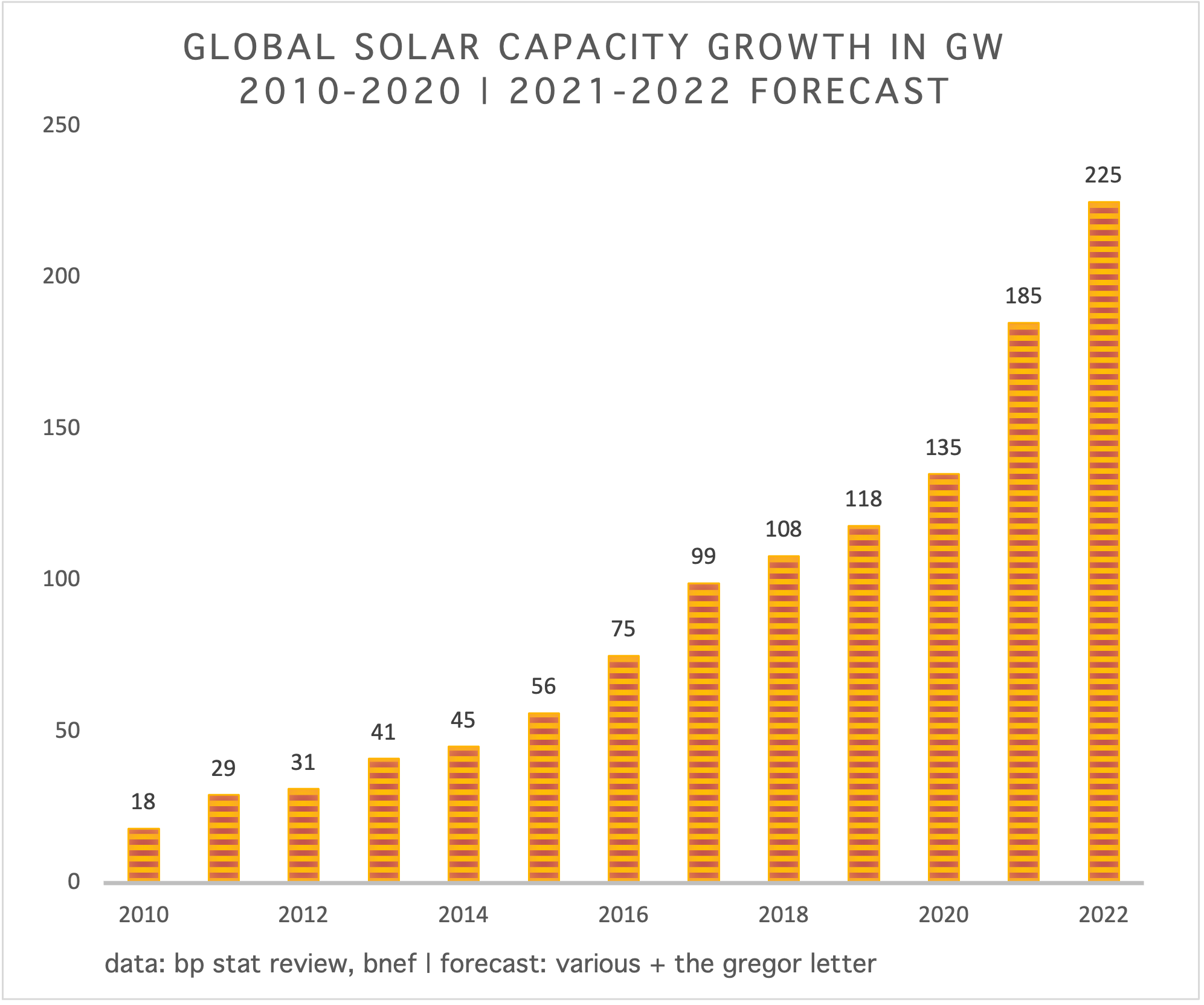

The Gregor Letter is raising its forecast of next year’s solar growth from the current consensus average of 205 GW, to 225 GW. Global solar, measured in capacity terms, is expected to grow a very substantial 37% this year, from 135 GW in 2020 to 185 GW. Now, the general rule is that years of such great leaps are followed by slower years. But not so slow as to fall to just 10% growth. With the US back in the game on climate policy, the EV adoption curve steepening, and the total disinterest globally in building new coal-fired power generation, solar is not just the cheapest and fastest source of new power but is about to go viral. It’s a lay up therefore that global solar will grow at least 20% next year, and the forecast of 225 GW in 2022 is probably conservative. Most experts just five years ago thought we were roughly 7+ years away from the first 100 GW year. Now, just six years later, we are looking at the first 200 GW year in 2022.

As you examine the chart, note the doublings are starting to unfold with some regularity, in four-year periods. While astonishing, 2025 may see the first 400 GW year.

Digitization, artificial intelligence, and the ability to duplicate technology at fast rates are key capabilities that everyone in the energy sector should now ponder. First, let’s start with a quote from The Selfish Gene, by evolutionary biologist Richard Dawkins:

The fundamental unit, the prime mover of all life, is the replicator. A replicator is anything in the universe of which copies are made. Replicators come into existence, in the first place, by chance, by the random jostling of smaller particles. Once a replicator has come into existence it is capable of generating an indefinitely large set of copies of itself.

Learning rates are a human created phenomenon that perfect and accelerate production and its efficiency. They are the process by which humans get very good at making copies of things, whether it’s lawnmowers, radios, or liquid-crystal displays. As the British physicist David Deutsche has observed, humans are capable of nearly infinite discovery and creation, as long as these pursuits are bounded by the limits stipulated by physics. Wherever physics makes endeavors possible, all that’s required is for humans to foster the conditions under which society can pursue them.

Now let’s consider the photograph below, in which a scannable QR code appears in the night sky over Shanghai. This is an advertisement for a technology company, and the code leads to their website. But that’s not the important feature of this display. The real question is: how was the airborne image launched and maintained in the night sky, to a degree of precision that would allow a mobile phone to capture it as code?

The answer: drones. That QR code image is created by a swarm of flying drones programmed to hover at a specific point in space to create a vertical display, with a high degree of precision. You are surely wondering, how does this apply to energy?

Well, let’s consider this time-lapse video of a jack-up ship installing wind turbines in 2018, at Vattenfall’s wind farm, off the coast of Scotland. In a very short span of time, human innovation has found a way to perfect and streamline offshore wind farm deployment, flipping its economics from an unprofitable to a profitable state. Aided by software, this is the hardest of hardware imaginable, in the uncontrollable domain of the sea, with all of its weather. The North Sea, no less.

When you see, therefore, annual global solar deployment moving rather quickly from 50 GW, to 100 GW, and then 200 GW it might behoove one to ponder that the automation of renewables energy deployment is inevitable. Those North Sea jack-up vessels are surely already integrated with software-enabled instrumentation and stabilization control, but there really is no limit to further automation. We are likely to see robot-aided deployment of both wind and solar proceed rather quickly in the years ahead. There is no reason why machines can’t entirely handle the job of utility-scale panel construction on the flat terrain where large solar is typically sited. And eventually we will see wind-power deployment ships that are largely programmed. Indeed, oceangoing freight shipping is already moving towards automation.

Marc Andreessen has famously said that software is eating the world. In energy, we should begin to consider that software driven automation will begin to define that world. Electricity itself will be routed, calibrated, stored, and even created also through precise automation. Moreover, such automation will drive costs to even lower bounds, thus making the overbuilding of wind and solar capacity not only possible, but optimal. Our current concerns about variability will seem quaint. A future energy system will have myriad backups, the exact opposite of today’s expectations. As with nature, humans will use technology to make copies.

Summer across the US West is shaping up to be hot, dry, and full of fire. The latest outlook from NOAA sees the entire US experiencing above average temperatures, and much of the West will see lower than normal precipitation. More bracing is that Colorado River reservoir water levels are already low, and will reach historically low levels as we move forward into the hot season.

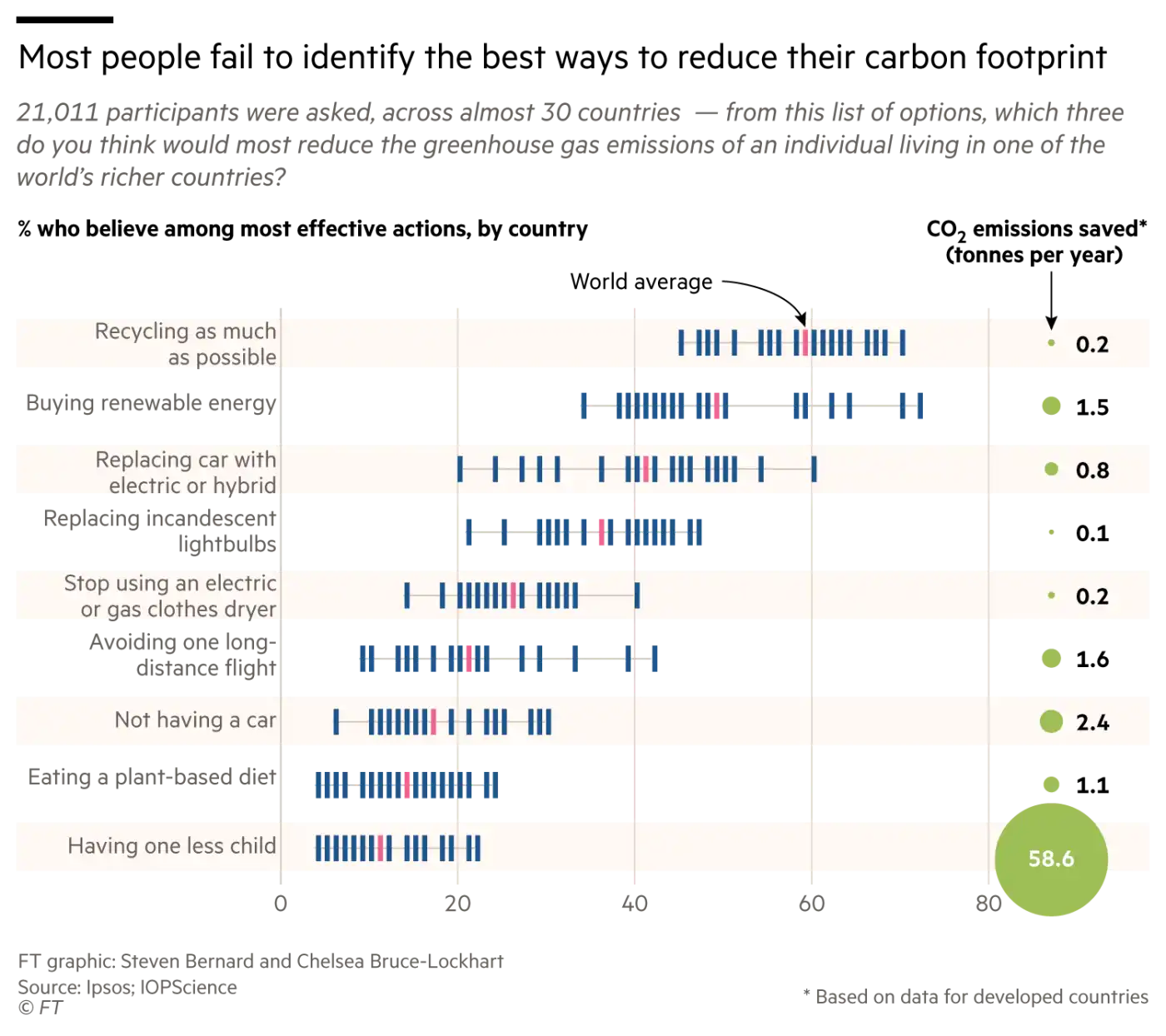

Most people fail to correctly identify the best ways to reduce their carbon footprint. A global survey of over 21,000 people was commissioned by the Financial Times to produce the results. Most striking is the spread between the choice to recycle, and the choice to not have a car. Most respondents thought recycling would have the greatest impact, and placed car ownership near the bottom of effects. The truth is quite the opposite of course. Polling data such as these nearly always confirm a similar result: no matter how informed individuals may be, broader society is often far behind in understanding of complex issues. If you already understand the impact of the global vehicle fleet, there is much work to be done before most share your view.

—Gregor Macdonald, editor of The Gregor Letter, and Gregor.us

The Gregor Letter is a companion to TerraJoule Publishing, whose current release is Oil Fall. If you've not had a chance to read the Oil Fall series, the single title just published in December and you are strongly encouraged to read it. Just hit the picture below.