Clean It Up

Mass timber, an emerging construction method, could potentially restrain demand for architectural steelmaking. In 2018 a new condominium in Portland, Carbon 12, became the tallest building in the US to be completed using such methods. Portland is also host of the annual Mass Timber Conference, an indicator that advances in cross-laminated timber engineering are creating new possibilities in building efficiency and design. (pictured below: mass timber bridge, from Nordic Structures).

There’s a broader claim being made however, by some mass timber advocates, that stepped up use of lumber could act as a meaningful contribution to carbon capture. The idea here is a kind of double bottom-line effect: that increased use of wood not only starts to displace steel, but accelerates reforestation thus growing the size of earth’s carbon sink. That possibility, at least in the near term, seems more dubious. Put differently, the notion is right but the scale and timing is wrong. Use of mass timber would have to increase not just a little, but a lot, to start a new demand pull on the lumber market. And it would take a decade or more to really harvest those benefits. Overall, this highlights the harder work decarbonization faces in the domain of construction, and industrial processes. Heating, steelmaking, and cement in particular remain tough nuts to crack.

Cleaning up the global electricity system is starting to move quickly, because doing so is affordable. That’s the main message in my interview last week with Joe Weisenthal and Tracy Alloway on the Odd Lots podcast from Bloomberg.

Arizona Public Services is the latest US utility to shock the power market with a sudden retirement schedule for existing coal assets. APS is the same utility that announced last year it would build storage instead of new natural gas generation, realizing it could arbitrage cheap surplus solar coming off the grid in neighboring California. Now, APS joins NIPSCO of Indiana, PacificCorp of Portland, Xcel of Minnesota, and Tri-State of Colorado in plans to shut down loss-making coal power. As I mentioned in the Bloomberg podcast, these utilities are running Monte Carlo simulations and discovering that, because new wind and solar are so cheap, they can now amortize the losses of shuttered coal and thereby deliver savings to customers. If readers are familiar with the final collapse path that coal took in the UK, it now appears the US is set to follow a similar trajectory.

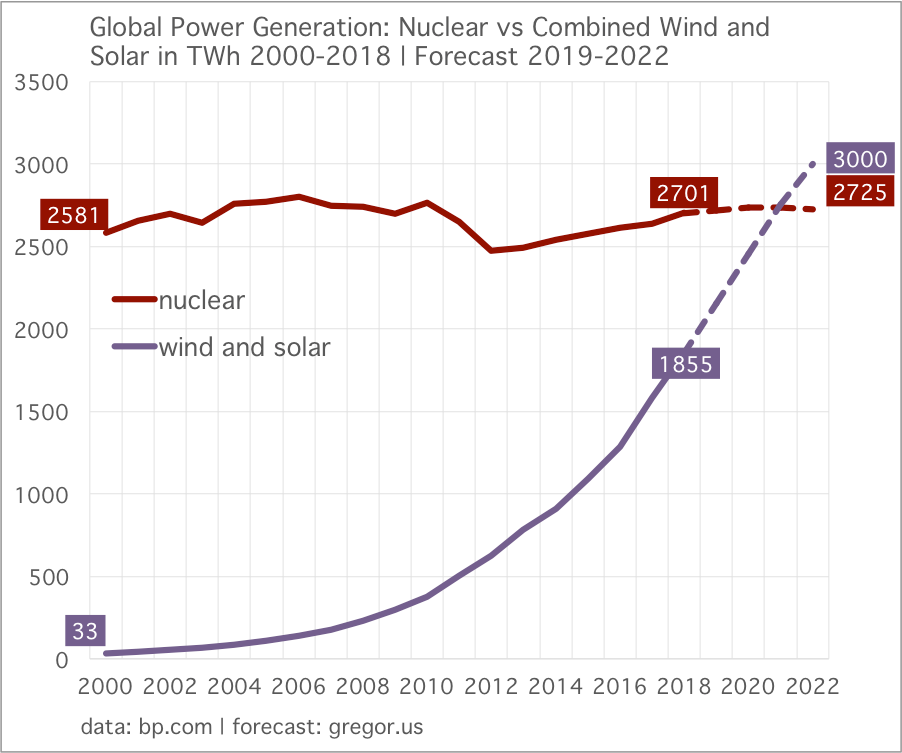

Combined wind+solar generation will start to overtake nuclear power globally, late next year. The imminent crossover is a testament to wind and solar power’s deployment speed, and affordability. But, this is not entirely good news for decarbonization as whole. Many domains around the world will still need some nuclear power, especially where populations are dense and land is expensive. In the chart below, retirements of existing nuclear largely offset new construction (mostly in Asia) which at least gives the world a flat nuclear generation outlook.

Here’s what’s bad: every terawatt hour of new generation from wind and solar is fated to lose traction each time we subtract a terawatt hour from nuclear. If you adhere to the view that climate actions taken now are multiplied through future effects, then you should at least want to hold the line on existing nuclear capacity—when possible. Here is what I wrote on this subject last year:

Ironically, it may be the very real success of wind and solar deployment that opens up a better argument for nuclear: as marginal amplifier, to make current progress move even faster. Here, we see that the cost argument has two sides. Yes, nuclear is now the most expensive new generation out there, and its ROI is second-rate, given its long construction timelines. But so what? As estimates of future climate-change damage ratchet upward, we should care less about up front price tags and more about outcomes that bear heavy losses. Moreover, although combined wind and solar are now moving very rapidly, and even with storage solutions also now emerging, in many domains the gaps in needed supply are being furnished by new natural gas. And natural gas, while far better than coal, will stand as a new emissions barrier in the years ahead.

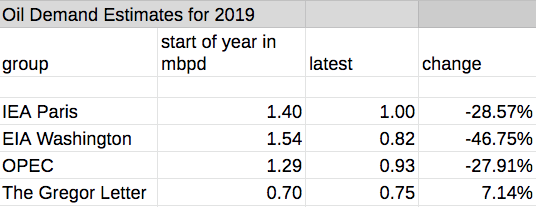

IEA Paris, EIA Washington, and OPEC are still on the back foot, scrambling to fit 2019’s far weaker oil demand into their previously high forecasts. Projecting that 2019 oil demand would be far weaker than expectations, however, did not require any special insight. All you really needed to know was that China’s car market was getting worse, the trade war was still a problem for global growth (especially in Europe), and that OECD demand was on a well established, stagnant pathway.

The most recent estimates from EIA Washington and OPEC have finally come closer to reality. But IEA Paris continues to stubbornly cling to the view that 2019 growth will end up near 1 million barrels per day (mbpd). That’s not going to happen and others are noticing. Allyson Cutright at Rapidan Energy Group in DC flagged the same ongoing problem also cited by the Gregor Letter more than once last year: each month that IEA refuses to lower its demand forecast, it then must rely on a higher demand rebound in the remaining months to make their target. Now it’s too late.

Why does 2019 still matter? Because 2019’s final level will form the baseline for 2020 estimates. As Cutright noted in her group’s report, hopes for a more balanced market in 2020 are already fading as a result. (And this was before markets began to react to the risk of economic disruption due to the Coronavirus, in China). To conclude, The Gregor Letter estimates that 2019 oil demand finishes up just 0.75 mbpd, the weakest in several years. 2020 doesn’t look much better.

Of note: while EIA Washington is quite bad at estimating global demand, it’s US forecasts are pretty good. In the most recent Short Term Energy Outlook report, US gasoline demand is expected to be flat again for the next two years, after failing to grow the past three years.

California’s solar mandate has now come into effect, requiring all new homes to be topped off with solar panels. My prediction is the policy will spur prefab and modular construction methods, in which the roof area itself is increasingly optimized for panel size. An early example of this approach can be seen at the Grow development on Bainbridge Island. In Europe of course, integrated solar design is already being standardized, and innovated. (Below is an example from Sweden). From a systemic change view, it’s not so much that large volumes of power will be produced from domestic rooftop solar. Rather, the effects will be felt in two other ways: through the suppression of demand growth for electricity, and more importantly, through the uptake of small scale storage either through neighborhood microgrids, or EV charging at home. Always remember that EV will be part of the storage solution.

Oil Fall, published early last year, will receive a major supplemental update this Spring. Most global data series on EV sales, electricity, oil consumption, and deployment of renewables will finalize in the next month or two. Accordingly, I’m preparing an update that will not only incorporate this data, but will address other developments. To name a few: the rise of global electrics as led by e-bikes, the woeful signal about future oil demand coming from the oil and gas services sector, the tipping point between the peak of ICE vehicle sales and road fuel demand, the mixed growth story of electric vehicles in major domains, the coming second-wave of utility scale wind and solar, and, the potential for new hits to oil demand growth from climate policy edicts, like a ban on plastic bags.

Single-use plastics (SUP) may seem like a trivial component of global oil demand, but not when a country the size of China bans them. As readers know, the oil industry is counting on growth in petrochemicals and plastics to keep oil demand steady. BP’s current long-term outlook for example indicates that 90% of the demand growth they expect to the year 2040 is over and done by 2025. In truth, the industry is holding out hope not for growth, but that other petroleum applications will prevent outright oil demand declines.

The Chinese ban on SUP, therefore, represents a significant threat to the petrochem-demand pillar, especially if copied across the Non-OECD. Interestingly, BP—in the same outlook cited above—understandably broke out a case analysis on SUP, and projected the hit to oil demand should bans get underway. BP’s conclusion? That a broad CPU ban could remove 4 million barrels a day of future demand (year 2040) from the entire oil market, after ripping the heart out of sectoral demand growth in petrochemicals.

There will be more analysis coming on the impact from the SUP ban. We should retain some skepticism before we get actual data from China (later in the year) on the scale at which the ban is actually adopted. In the meantime, please see this excellent analysis from Liam Denning at Bloomberg. A juicy tidbit: the Bank for International Settlements has written a report that coins a handy phrase—green swan—to describe the looming risk that sudden policy shifts, driven by climate concerns, could present ongoing challenges to incumbents in every sector from fossil fuels to transportation.

—Gregor Macdonald, editor of The Gregor Letter, and Gregor.us

The Gregor Letter is a companion to TerraJoule Publishing, whose current release is Oil Fall. If you've not had a chance to read the Oil Fall series, the single title just published in December and you are strongly encouraged to read it. Just hit the picture below.