Art of Oil

Dustin Yellin, the artist, has built a flourishing art community in Red Hook, Brooklyn through a patient renovation of overlarge, civil-war era industrial buildings. His latest project, however, will require a more ambitious use of construction engineering. As reported by Rob Cox at Reuters BreakingViews last week, Yellin, wishing to make a statement about climate change and fossil fuel consumption, proposes to stand a 1000 foot ship known in the industry as a VLCC—a very large crude container—on its head, bow firmly planted, and the stern with its control tower in the sky.

The personal connection to climate change would be obvious to anyone who’s followed Yellin’s work over the past decade, as his stunning rehab of the 24,000 square foot Time Moving and Storage building near the Red Hook waterfront, begun in 2011, was dealt a damaging setback through flooding from Hurricane Sandy in 2012. Yellin’s ongoing project recovered strongly, however, and today operates as Pioneer Artworks, a community exhibition space. (see my own photo of the interior, from 2017, below)

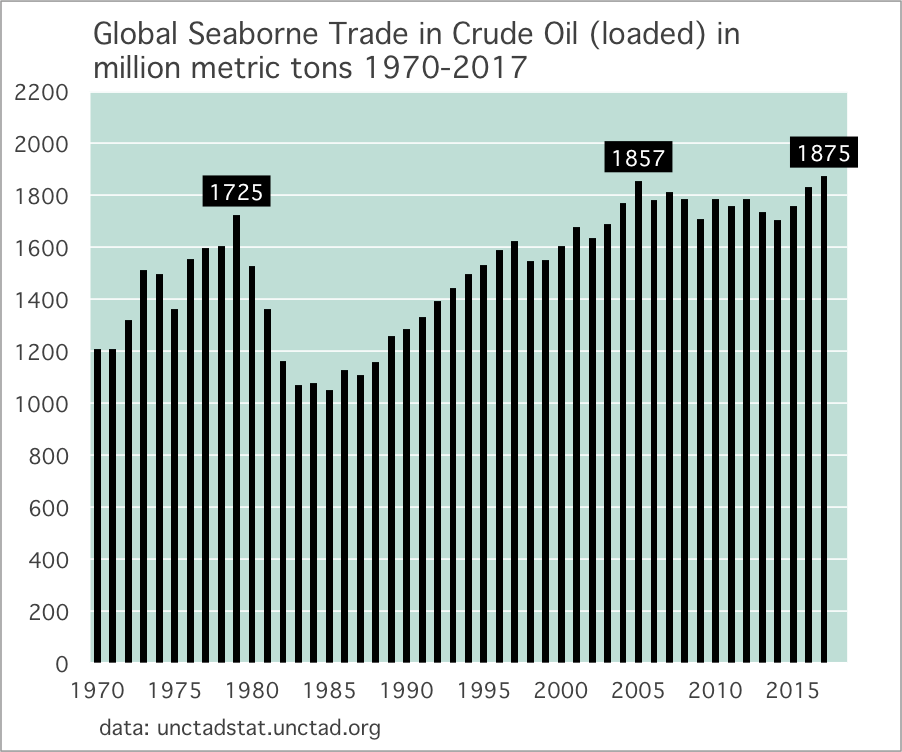

Yellin’s fascination with the crude oil tanker itself, a vessel in both literal and metaphorical terms, got me to wondering whether his artistic impulse was intuiting something timely, about the global shipping of oil. So I pulled recent data from the United Nations Conference on Trade and Development (UNCTAD), and it indicates that, just like the growth rate of global oil consumption, the seaborne trade of oil has slowed markedly, since the strong 20 year growth period from 1985-2005.

While it’s true the ascent of the US, as a relatively new exporter of crude oil and petroleum products, is a trend that will surely extend into the future (especially when US oil consumption enters decline) the brake on global oil consumption growth began some years ago, and will accelerate during the 2020-2025 period as EV adoption enters the rich portion of the adoption curve.

Seen in one way, Yellin’s upright VLCC is both a protest and a wish, but looked at from another angle, may turn out to be a decent prediction, a classic one, typical to a phase transition in the oil market.

Bloomberg New Energy Finance released its latest global EV outlook and I’m not sure it’s quite aggressive enough. Mind you, BNEF has been more consistently right, and more aggressive, than most other institutional forecasters—especially when compared to the very poor, almost comical forecasts from EIA Washington and IEA Paris. What’s BNEF’s edge? They have a heavy presence in China, the epicenter of global EV adoption in both passenger vehicles and buses. Moreover, BNEF incorporates a projection of cost curves and increasing EV affordability into their outlooks, as you do. This may sound rather standard, but in many forecasts that tend to undershoot (and even overshoot) the rate of EV adoption, there is insufficient attention paid to how quickly the sticker price of EV will begin to compete head-to-head with comparable ICE vehicles—even as the TOC of EV (total cost of ownership) is already competitive. Most important of all: BNEF and I are in complete agreement that the growth of passenger ICE sales has likely peaked. So the discussion from this point forward needs to center on the rate of EV adoption, and the forecast of the size of the total annual market.

The figure I’d like to push back against, in BNEF’s model, happens to be the number that’s furthest out in time: that 57% of passenger car sales will be electric, by the year 2040. At first glance, it might appear to be more useful to readers of The Gregor Letter to dispute a level or rate much nearer in time. After all, much is going to unfold in the next five years, and while we certainly care about middle century targets, from a climate perspective, they are deeply uncertain. But follow me for second…

I’d be surprised if ICE (internal combustion engine) sales are above a 10% market share in the year 2040 for passenger cars, frankly. And even that low level assumes some corner of the industry will have enough supply chain support to continue producing them. Perhaps ICE passenger cars will become a bespoke endeavor by 2040, filling a niche of market demand at presumably higher prices—a reflection of a product that has lost its economies of scale. If you’ve ever been to London, for example, and sampled the extraordinary preservation of historic craft in men’s haberdashery, such artistic cultivation might be a model for future ICE passenger cars. Perhaps in the year 2040 you’ll be able to custom order a 3D printed 1967 Shelby Mustang with a V8 engine. And perhaps Ford and other legacy automakers will have a tiny little side-business in licensing these patented designs to a small custom-build ICE auto industry. But why would the industry itself bother with ICE? The primary drivetrain in sales, even by BNEF’s admission, will be EV by the year 2040.

So here’s what I’m suggesting: work backwards from there. Most forecasts indicate EV sticker prices go head to head with ICE by 2022. If so, that suggests the market (already flipping in China, by the way) is going to turn so hard towards EV that BNEF’s forecast of a 57% EV market share is more likely to come true ten years early, by 2030.

We should also pay some attention to the denominator. BNEF has of course weighed in on how large the passenger market might be in the year 2040, and tipped its cap to car sharing services, autonomous vehicles, and the expected tail off in personal car ownership. But I have to wonder: will this still be a 100 million unit market, by the year 2040? I will leave that as an open question, but as you will agree, a forecast of the total market greatly impacts the EV and ICE market share percentages.

One sweet little tidbit in the BNEF forecast that has less to do with market share numbers, but which should be relished nevertheless, is the observation that EV are going to displace more global oil demand than BNEF previously expected, in part, because the future pathway of efficiency gains in ICE fuel economy has recently shifted, downward. I mean, that’s just delicious. Efforts to relax fuel consumption regulation, a pointless and stupid policy as seen here in the US, will accordingly result in a harder impact on the oil market from EV adoption, as regulatory capture gives a short-term boost to the auto industry, that will hurt the oil industry. All I can say is: chef’s kiss.

The IEAs latest Oil Market Report indicates the slowdown in China’s road fuel demand continues. As readers may recall, China’s consumption of gasoline and diesel/gasoil fell atypically last year by about 1.00% against a backdrop of a quickly deteriorating vehicle market, which abruptly fell apart in the second half of 2018. Through the first four months of 2019, China’s combined road fuel demand fell harder than last year, however, prompting the IEA to shift downward its full year forecast from a small increase of just 0.3% to another decline of 1.00%. Of course, the IEA is ever bullish on global oil demand generally, which has seen the direction of its revisions swing more concertedly to the downside. They are now forecasting China’s overall oil demand will grow again this year, by just a touch less than last year, despite the slump in road fuel.

The problem with the forecast is that China’s car market continues to slide and the economy overall is weaker. While the IEA acknowledges the downside risk to their forecast, depending on the outcome of the trade war, they are as usual anticipating a recovery in oil demand in the second half of the year, even though the vehicle market is already down 12.2% now, year-over-year, through the first four months of 2019. The IEA should have started pricing in the damage coming from the trade war now, not later, instead of holding out for a happy resolution.

A better forecast would be that China’s road fuel demand will fall by well over 1.00% this year, and on my own spreadsheet I’ve penciled in a decline of 2.4%. Why? Because China’s vehicle market only started falling apart in July of 2018, and managed to finish 2018 down “just” 2.76%. This year’s pace of 12.2% will surely improve a little, but I’ve priced in an 8.00% -9.00% decline this year. Combined with EV sales, which continue to power forward at a 60% growth rate, it seems pretty clear China’s total oil demand will grow more slowly this year.

In the big picture, the February letter laid out why I thought the IEA’s 2019 forecast of 1.4 mbpd of global oil demand growth was also too high. My forecast remains: that global oil demand will grow instead by less than 1 mbpd this year, closer to 0.7 mbpd. While the May Oil Market Report from IEA only adjusted their forecast down a tick, from 1.4 to 1.3 mbpd, we can start to have some confidence they’ll have to revise downward (as usual). Oh, and by the way, data from EIA in Washington shows that not only is US gasoline not growing again this year, for the third year in a row, but total oil demand itself in the US has also gone flat. And the US car market is also weakening at a stronger pace than last year.

By the time we reach the end of 2019, China will have sold about 2 million less ICE vehicles than last year, while EV sales will grow by 2 million. That, dear reader, is a high resolution portrait of the future, now heading toward us at considerable speed.

—Gregor Macdonald

The Gregor Letter is a companion to TerraJoule Publishing, whose current release is Oil Fall. If you've not had a chance to read the Oil Fall series, the single title just published in December and you are strongly encouraged to read it. Just hit the picture below.